Photo by m. on Unsplash

Photo by m. on Unsplash

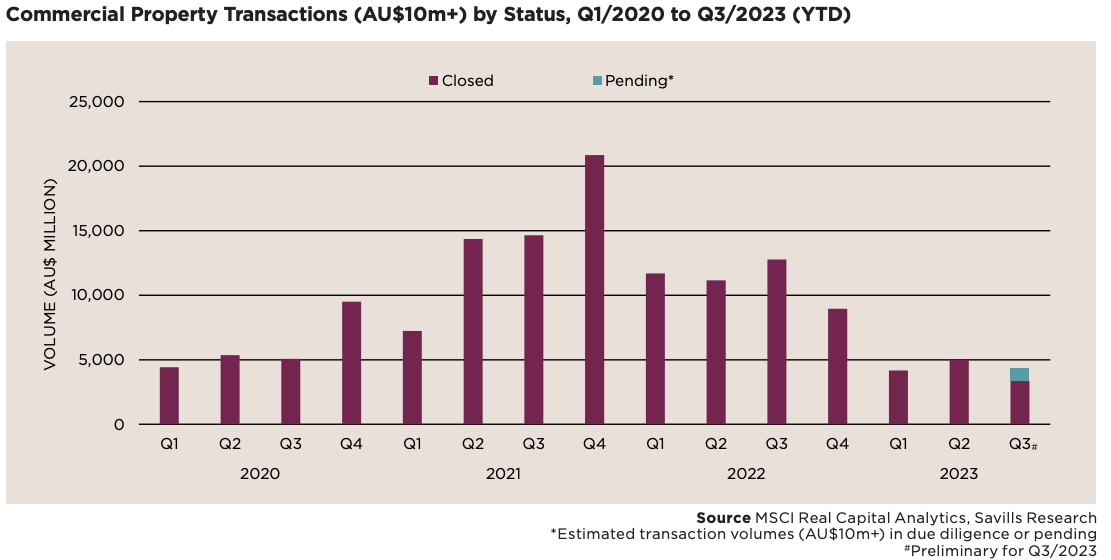

Australia real estate investments drop 33% to AUD3.3b in Q3

Preliminary estimates show industrial outperformed other sectors with investments worth AUD1.5b.

The impact of higher inflation and interest rates continue to dominate decision-making in Australia, although there are very early signs that the economy is at a turning point, according to a recent report by Savills.

Overall price inflation has continued to decelerate, led by goods, but remains high due to services price growth, similar to overseas economies. Wage growth, which has been quite strong over the last three quarters, has eased slightly, even though the labour market remains tight. However, unemployment has started to trend higher, and underemployment has ticked up slightly.

Here’s more from Savills:

Higher interest rates are weighing on consumer spending, particularly for discretionary goods. However, the Australian economy is being supported by a strong rebound in net exports and a faster than expected recovery in population growth due to a rebound in net overseas migration. Global and domestic headwinds will drag on activity in 2023 and 2024, although the Australian economy is expected to outperform other major advanced economies.

The RBA has kept its interest rate unchanged for four consecutive months, with the long pause suggesting that Australia’s central bank may be approaching the end of its tightening cycle. Most economists are still expecting one more rate rise later this year. While central banks are near the end of the tightening cycle, expectations around timing of monetary policy easing have been pushed back well into 2024. The continued pause, however, is being welcomed by investors.

Investment activity remains subdued relative to the record volumes transacted during the previous two years. There has been some repricing, as yields continue to expand outwards across office, industrial and retail. However, constrained transactional activity is limiting price discovery, particularly for office, while rental growth in industrial continues to partially offset its revaluations.

As the interest rate outlook becomes clearer, the bid-ask spread between buyers and sellers will narrow. Despite the uncertain outlook, a number of major deals closed during Q3 and there are several in the pipeline, suggesting liquidity has improved for some buyers and sectors. Opportunistic capital has been active, alongside syndicators, select institutions and offshore groups. The preference for global capital to increase exposure to Australia will continue to play a significant role in unlocking investment activity.

Preliminary estimates for Q3 indicate that investment volumes across the office, industrial, and retail sectors (AU$10m+) fell 33% in quarterly terms to c.AU$3.3 billion, down from c.AU$4.9 billion in Q2/2023 (excluding transactions that are in due diligence/pending). By sector, office volumes are at c.AU$1.1 billion, similar to Q2 at c.AU$1.13 billion. Industrial is currently at c.AU$1.5 billion, down from c.AU$2.1 billion in Q2. Retail volumes are at c.AU$706 million, down from c.AU$1.7 billion in the previous quarter.

Advertise

Advertise