4 reasons why APAC corporates are selling their real estate assets

There were 762 deals worth over USD40 billion completed in 2021.

The pandemic caused corporates to find ways to strengthen their balance sheet amidst the uncertainties and various disruptions. One of the ways they did this was to sell their real estate assets, causing real estate disposals in Asia Pacific to surge to record highs in 2021.

According to data from CBRE, 762 deals worth a combined total of US$44.4 billion were completed in the region in 2021 as sellers capitalised on strong pricing to offload assets.

CBRE enumerates four key reasons behind companies’ “selling spree”:

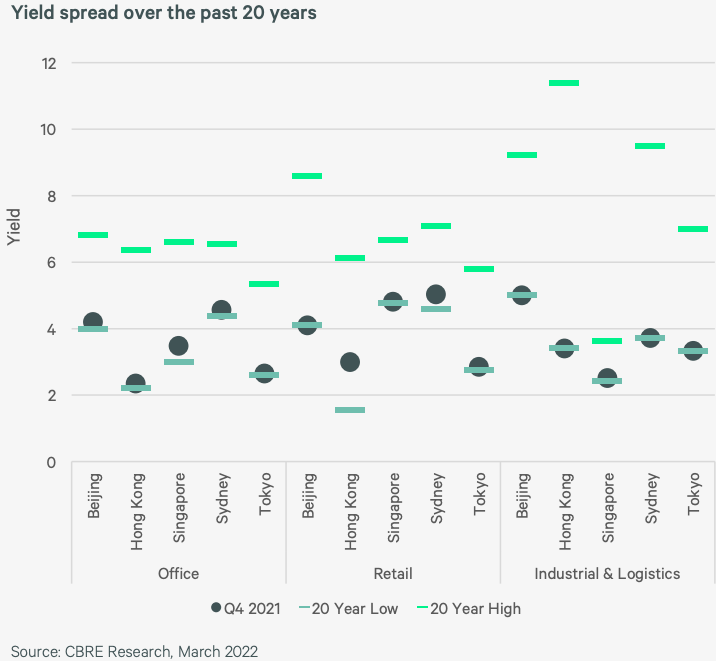

1. Positive market conditions

Asia Pacific commercial real estate has performed well throughout the pandemic, with pricing across most geographies and sectors close to record highs as of Q4 2021. With almost every market in the region at or within 50 bps of the 20-year low yield, these upbeat pricing conditions are encouraging corporates to sell down their real estate assets.

2. Portfolio optimisation

The pandemic has prompted corporate real estate occupiers to review their operational footprint across leased and owned portfolios. Many corporates have subsequently implemented portfolio optimisation strategies, which has resulted in the identification of self-owned facilities, particularly in the industrial and manufacturing sectors, that are no longer fit for purpose. This has been the catalyst for corporates to plan strategic exits either via short-term leasebacks or vacant possession disposals.

3. Increasing liquidity

With yields remaining elevated across Asia Pacific, corporates have taken the opportunity to liquidate their real estate holdings to increase cash on hand for their core business. Corporates are recycling capital generated from asset monetisation as they are either seeing higher returns in their core business or require funds for M&A.

4. Enhancing profitability

Many corporates have identified opportunities to book a gain on sales via asset monetisation as an avenue to simultaneously raise capital and enhance reporting profits. While other debt solutions may be just as economical as asset monetisation, these traditional forms of debt do not enable corporates to enjoy the upside of profit enhancement.

Even despite the latest lease accounting standards (IFRS16 & ASC 842), which require all corporates to record lease liabilities on their balance sheet, corporates increasingly view sale leasebacks as an alternative and more efficient way of raising capital while enhancing profits.

Advertise

Advertise