Singapore Grade A office rents to increase 5.4% this year

Grade B office rents are likewise expected to grow by 2.7%.

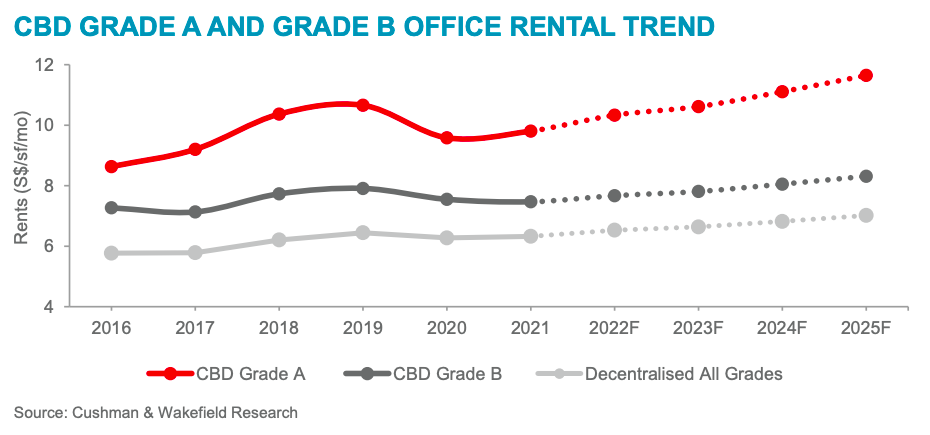

Singapore office rents are expected to trend upwards as firms continue to work towards flight to quality. According to a report from Cushman & Wakefield, CBD Grade A and Grade B office rents grew 3.7% and 0.9% respectively in H1 2022 YTD.

“Supported by the return-to-office momentum and pick-up in business activities, CBD Grade A and Grade B office rents are forecast to grow by 5.4% and 2.7% y-o-y for the whole of this year amidst a tight supply situation,” the analyst said.

Here’s more from Cushman & Wakefield:

A flight to quality with increased focus on sustainability and workspace experience continues to drive demand for Grade A offices. CBD Grade A office rental growth may slow in 2023 (rent growth about 3% yoy), as occupiers take a more cautious approach in a heightened interest rate environment.

Decentralised office markets that enjoy lower rents may see more demand going forward, as occupiers become more cost-conscious, though this would be led by Grade A offices. Rising rents and redevelopments in the CBD could gravitate demand towards the lower-priced decentralised markets. Decentralised office rents have risen by 1.5% in H1 2022 YTD and are poised to grow 3.2% y-o-y for 2022 and about 2% y-o-y for 2023.

Redevelopments to Tighten Supply and Bolster Demand

Overall office demand remains positive with CBD Grade A office vacancy rates expected to tighten towards 4.5% by end-2022 as net demand remains positive. Vacancy rates are expected to rise in 2023, with increased supply due to the expected completion of Central Boulevard Towers. Future supply remains tight. The CBD Grade A office supply pipeline is limited with 0.7 million sf (msf) of new stock per annum from 2022 to 2025, as compared to the ten-year annual average of about 1 msf.

Office supply in the CBD could also tighten over the mid-term as the flight to quality and programmes like the CBD incentive scheme prompt redevelopments. Also, the expiry of transitional office sites that might happen progressively over 2022 to 2026 may spur displacement demand of up to 0.8 msf. The push for redevelopment would drive more displacement demand over the short to mid-term, supporting office occupancy rates.

Advertise

Advertise